Indonesia’s forest carbon opportunity: a view in data (2025)

Indonesia sits at the centre of one of the world’s biggest nature-based climate opportunities. Its forests store enormous carbon stocks, support globally important biodiversity, and – crucially – are now backed by growing political momentum for high-integrity carbon projects. The potential is there. The question is: where does the opportunity lie?

To explore this, we produced a land-cover and carbon report analysing Indonesia’s land-use change and carbon potential over the past decade. Using audit-grade data, we mapped forest dynamics, measured carbon losses, and highlighted regions most suitable for conservation and restoration. The result is one of the clearest pictures yet of Indonesia’s nature-based solutions potential.

Forest cover and land-use trends

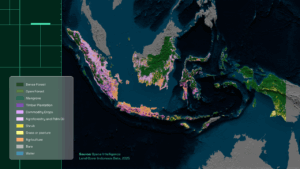

Indonesia’s forest estate is incredible – 61% of the country (112 Mha) is forested, storing roughly 100 billion tonnes of carbon, about 10 times the world’s annual fossil fuel emissions. But this is down from 80% in 1980, and the pattern of change varies by region.

- Largest forests: Papua (42.6 Mha), Kalimantan (37.1 Mha), Sumatra (18.5 Mha); Papua also holds 1.65 Mha of mangroves.

- Recent trends: Over the past decade, dense forest declined 3.8% (4.52 Mha), while non-tree agriculture (excluding plantations) fell 6.25% (1.44 Mha).

- Regional pressures:

- Sumatra: 1.04% annual deforestation, over 2 million hectares lost, mostly due to oil palm and industrial timber.

- Kalimantan: deforestation accelerated 1.5x over the last 5 years.

- Java: agriculture converted to high-value timber and oil palm plantations.

- Sulawesi: relatively stable, at 0.31% annual deforestation rate (2015-2025)

- Papua: largely intact forest but facing pressure from development, plantations, and road expansion.

- Sumatra: 1.04% annual deforestation, over 2 million hectares lost, mostly due to oil palm and industrial timber.

The pattern is consistent nationwide: forest loss follows plantation expansion.

The carbon potential picture

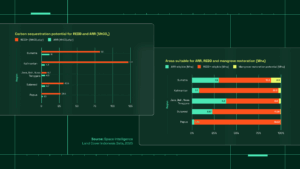

Indonesia’s total annual carbon potential reaches an estimated 299 MtCO₂ per year across 128 million hectares. Translated into action, this represents space for more than 800 high-integrity projects – with the right investment and strategy.

- REDD+: 267.7 MtCO₂/yr, concentrated in Kalimantan, Sumatra, Papua. These regions still hold large blocks of dense forest under measurable threats.

- ARR: 26.3 MtCO₂/yr, strongest in Java-Bali-Nusa Tenggara, Sumatra, Sulawesi. Carbon saturation rates of 15-50 tCO₂e/ha/yr make Indonesia one of the fastest forest-regrowing countries in the world – 7-10x faster than European or North American forests.

- Mangroves: 4.3 Mha area, 4.9 MtCO₂/yr carbon impact. Mangroves are high-impact, fast-payback ecosystems, with the biggest opportunities for restoration in Sumatra and Kalimantan.

On the future of Indonesia’s VCM landscape

Carbon and environmental policy in Indonesia is moving in the right direction. Under the new administration, Indonesia is reopening to global carbon finance and actively signalling that new high-integrity NbS projects are welcome.

Throughout 2025, Indonesia has signed mutual recognition agreements with the major global standards like Verra, Gold Standard, Plan Vivo and others. It’s clear that Indonesia is reopening fast and with high-quality land use and carbon data and MRV processes in place, the risk inherent in forestry projects can be managed more easily.

But operational hurdles remain:

- Land tenure is often fragmented and inconsistent.

- Smallholders generally prioritise immediate income over long-term carbon commitments.

- Traditional land management, including field burning in some regions, introduces permanence risks.

Next steps

Indonesia offers one of the world’s most significant opportunities for high-integrity forest carbon projects. Its forests can attract hundreds of carbon projects, protect globally important ecosystems, and deliver meaningful climate mitigation. But these opportunities sit within a complex landscape shaped by land-use pressure, local economics, and fast-shifting policy.

Download the full report to explore the numbers in detail.